UPI is the Unified Payments Interface which is a real-time payment system developed by National Payments Corporation of India (NPCI) and regulated by the Reserve Bank of India (RBI). UPI was launched in 2016 and has been very successful in allowing payments between consumers and companies. In fact, for the financial year 2021-2022 (April 1, 2021, to March 31, 2022), it crossed over $1 trillion dollars in transaction value via the platform.

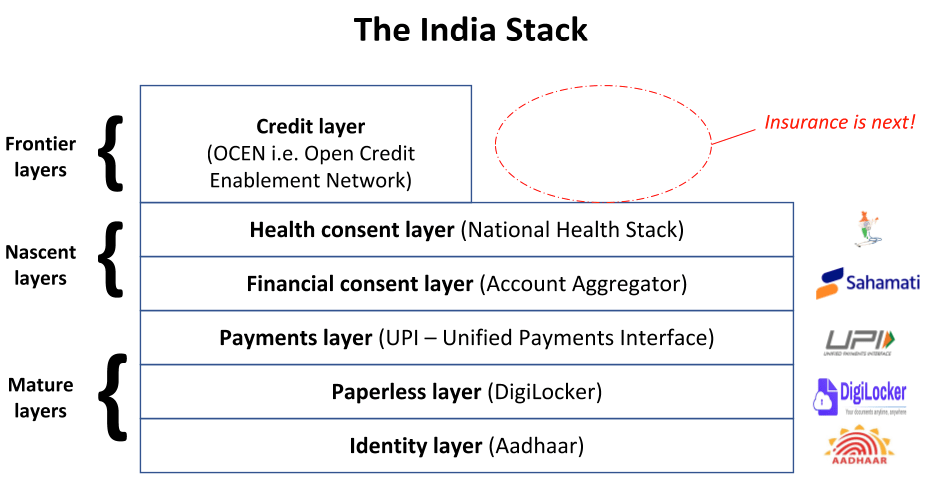

UPI is one of the building blocks for the India Stack, which is a set of open APIs to unlock identity, data, and payments in India. The growth of UPI can be tied to the government pushing it and also all the apps that enable it like PayTM, PhonePe, Google Pay, and many others.

It’s not often you can say that something beautiful has been created by the government but in this case, you can. The digital push by the Indian government has led to many jobs and industries being created. I would argue that Reliance’s Jio would not have been able to onboard 400+ million customers onto their platform if it were not for Aadhaar. Imagine the old method of paper documents, counter-signed photos, etc… Old skool identity authentication.

Although I use UPI several times a week to make payments I find the system still very broken. I envisioned a web dashboard or mobile interface that would show ALL my pending payments and then I could quickly accept/deny them. That’s not how it works for me today.

For example, when my car insurance renewal comes due I get an email with a payment link. I click on the payment link and then do a bunch of shit and it gets paid. Now imagine, this happens for most of the payments I have to make. Each has a different gateway, interface, or user flow and I have to jump through hoops to make the payment.

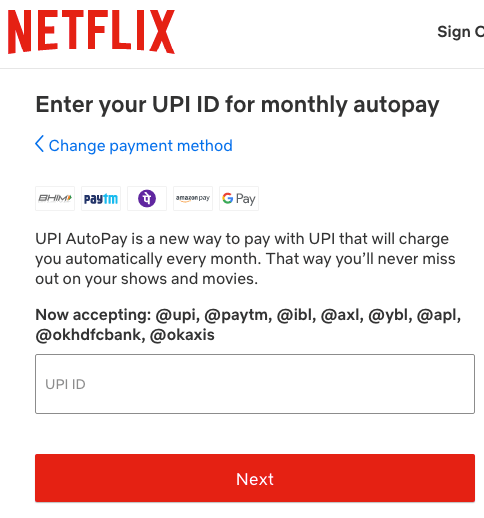

I thought I would provide these companies my UPI ID and they would push a payment request to me and I would go to my app of choice and accept or deny the payment request. Netflix is the first company that I have seen do this recently but I have yet to experience it. I hope more and more companies just ask for my UPI ID instead of sending me a payment link.

This process should also get extended to companies that also have to make payments. If a company provides their UPI ID and GST number, then the UPI transaction limit should be increased for them. This would solve a lot of credit card issues for companies that are using SaaS products or other tools from international companies.

Even though UPI is broken for me at the moment, I still love the ease of use to make a peer-to-peer payment. UPI is definitely here to stay and the numbers speak for themselves.