If you got married because of Shaadi.com, you can thank my brother-in-law Sandeep Jain and me. 30 years ago today, … More

Cars, technology, finance and fitness.

If you got married because of Shaadi.com, you can thank my brother-in-law Sandeep Jain and me. 30 years ago today, … More

I have spent 30+ years in technology. I have seen multiple waves of disruption: the internet, mobile, cloud, SaaS. Each … More

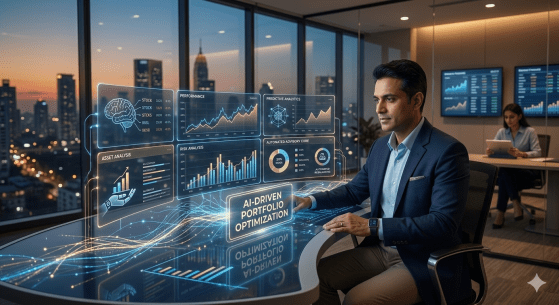

In the world of AI, everything is cool until it hits your area of expertise. I saw the recent announcement … More

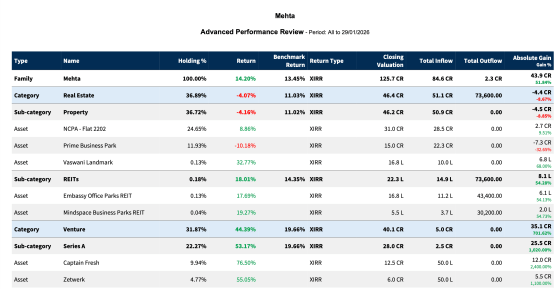

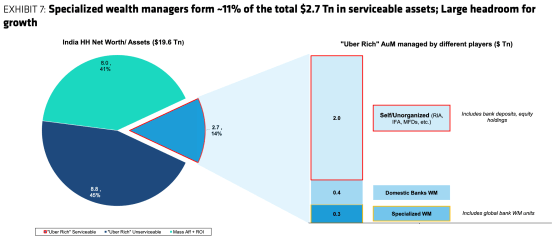

I was recently diving into a detailed report from Bernstein about the state of wealth in India, and one number … More

WARNING: Hard to believe but this blog post has nothing to do with cars! When you are starting something new, … More

Recently, MProfit took part in the Transformance Forums Family Office Summit in Bengaluru. It was a gathering of around 100 … More

Well, it finally happened: Tesla opened its first showroom in India, right in the business district of Mumbai called Bandra-Kurla … More

Yesterday, while I was in BKC (Bandra-Kurla Complex) for a meeting, I strolled past the construction site of what will … More

If you have been tracking my YouTube channel Electric Avenue you know I have taken a break, it was a … More