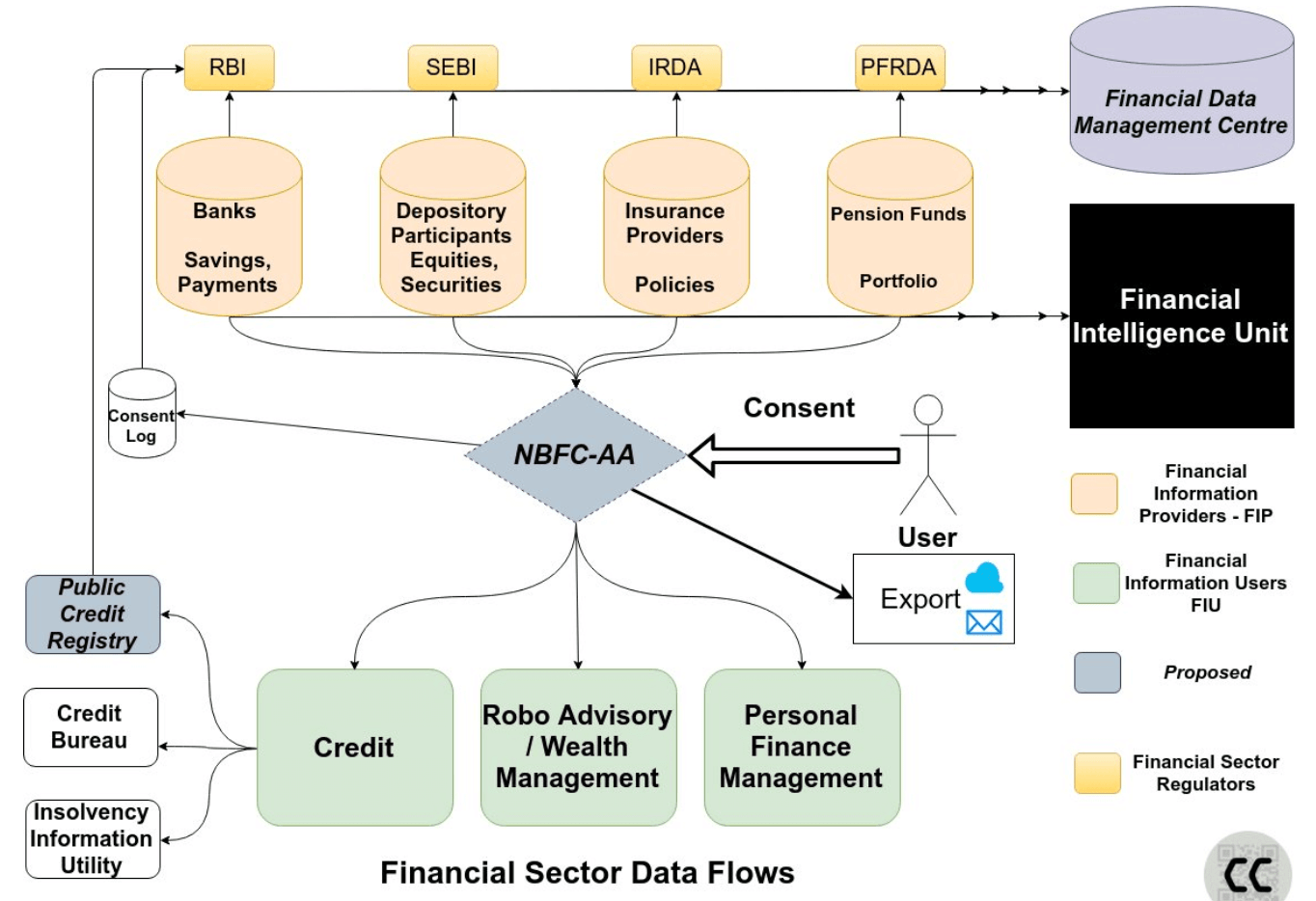

Since the official launch of Account Aggregator (AA) in September 2021, much has been written about what it can do. The quick elevator pitch of what AA does – it’s a financial data sharing framework that allows consumers to control who can view their personal financial data. The implications are big.

But, before we get into the specifics of what it can do, I wanted to write a bit about how we got here. The seeds of AA were planted in a September 2016 press release from the Reserve Bank of India (RBI). In the circular they talked about a new class of non-banking finance companies called Account Aggregators (NBFC-AA).

In addition to RBI, there were 3 other government agencies that were part of the initial team to aggregate financial information:

- Securities and Exchange Board of India (SEBI)

- Insurance Regulatory and Development Authority of India (IRDA)

- Pension Fund Regulatory and Development Authority (PFRDA)

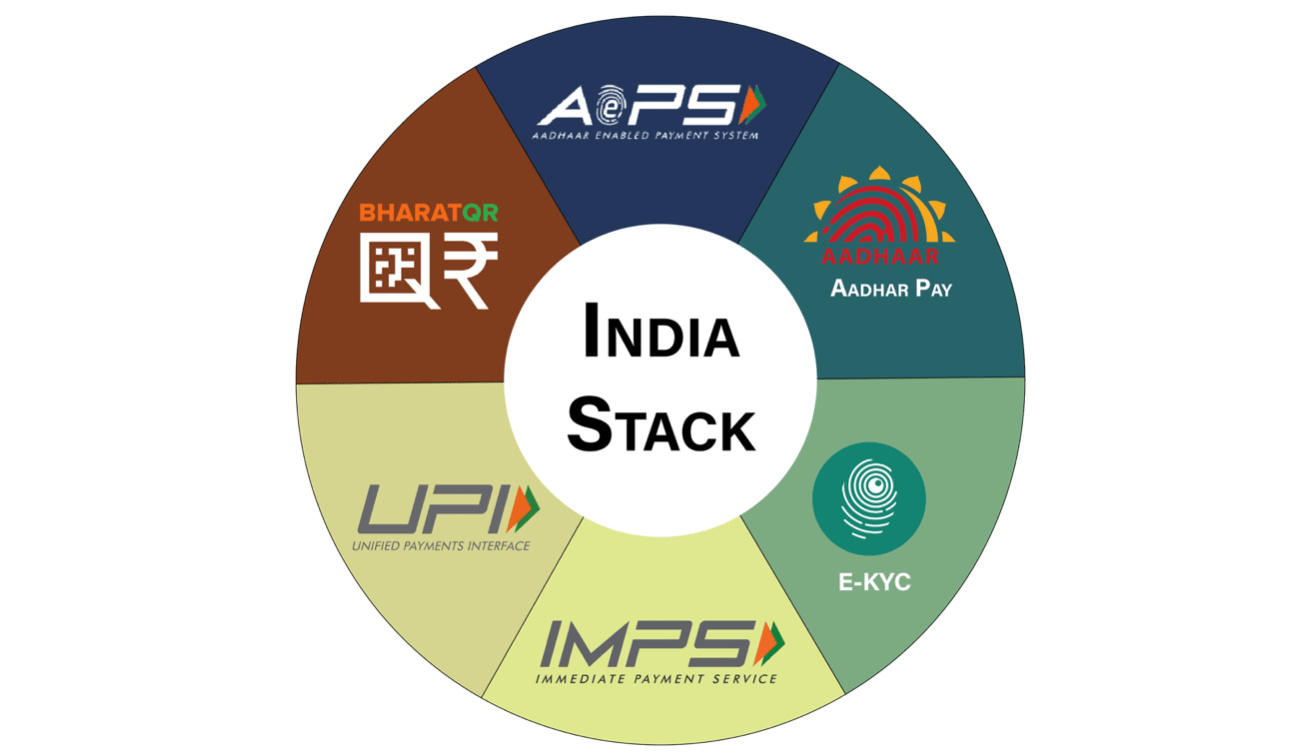

AA was launched to be a part of the IndiaStack which is India’s Digital Public Infrastructure (DPI), which includes AEPS, Aadhaar, e-KYC, IMPS, UPI, BharatQR, ONDC, and several other programs. When you got 1.3 billion people you need to move from paper based systems to digital!

Then in 2019, the technical specifications for AA were published by RBI. Of course, Covid hit and things slowed down. But, by September 2021 the government finally launched and opened up the AA platform.

One of the first use cases for AA was providing credit to SMEs by getting their banking and GST data and analyzing it. Since the data was coming straight from the banks and the government, there was very little chance the data could have been falsified and thus proper credit lending would benefit the SMEs.

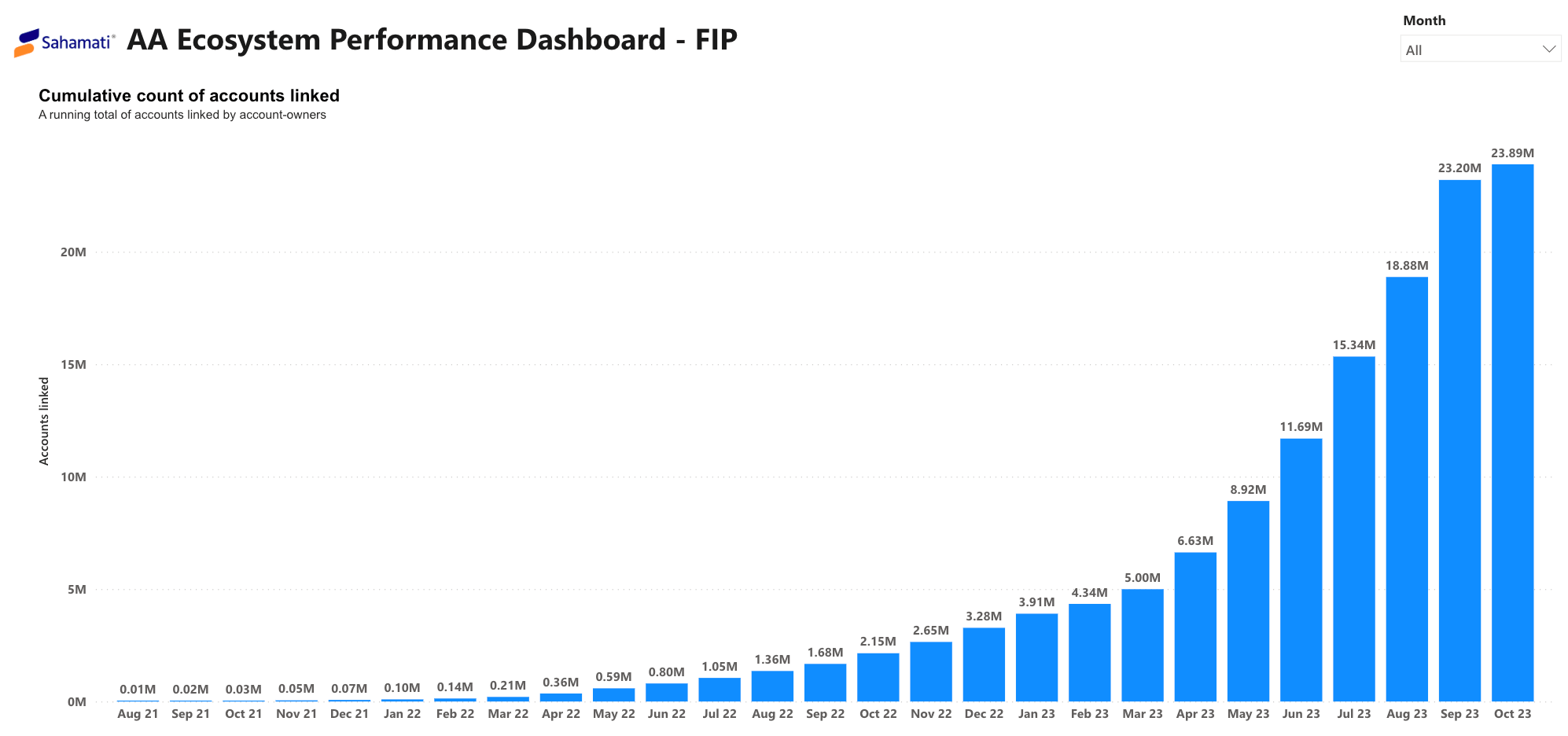

So how successful has it been? They say a picture is worth a thousand words, the graph below is what every startup/company dreams of…accelerated usage.

Another use case I have seen lately is providing a complete snapshot of all your investments in the securities market – equity shares, ETFs, mutual fund units, corporate bonds, government securities and other instruments held in your demat account. This is a great first step but it’s not a complete picture.

It’s similar to getting your blood reports from a pathology lab. If you look at that single report and not any other previous reports then you really can’t build a trend or pickup any irregularities. Now imagine you have the past 10 years of your blood reports, then it’s very easy for a doctor to see what your individual baseline numbers are and if there is anything highly irregular with certain values. Having the the full transaction history of all your financial transactions is the key and not just a single point-in-time snapshot.

As I mentioned, this is the first step and for many people they have NEVER even gone to a path lab to get their blood work done so this is a step in the right direction. I believe this will open up the door for more and more consumers to start using the services of advisors to get real value-add services…all thanks to the AA framework.